Valuing the Top 5 S&P 500 Stocks

Since this Sunday is Christmas Eve, I've decided to not bother you on that special day and post the weekly Sunday Episode a day earlier. I hope you like it and enjoy your Christmas Holiday!

Today’s episode is sponsored by Shortform

Today, we will quickly go over and value the 5 biggest stocks of the S&P 500.

The S&P 500 is the most important stock index in the world, and it features some of the most famous and powerful companies in the world.

In this series, I’ll regularly discuss 5-10 stocks and eventually go through the entire S&P 500. If you like that idea, like this post or write a comment to let me know!

I’m looking forward to learning a lot about new businesses and industries. The first dozen companies are probably well known. I’m sure this will change as soon as we get deeper into the S&P.

Today’s companies are:

Apple Inc.

Microsoft Corp

Amazon.com Inc.

Nvidia Corp

Alphabet Inc.

The graph below gives you a quick overview of how important the heavyweights are to the performance of the S&P. The seven biggest stocks of the index outperformed the rest by a huge margin.

I’m very proud to present Shortform as today’s sponsor!

This year, I read two new books every month. The hardest part is figuring out what books to read and prioritizing them.

Shortform helps me with this. I can check out the core ideas and principles of the book and then decide to invest the time and money to read the entire book.

And Shortform not only summarizes books, they also add insights and exercises to make sure you internalize the lessons.

Shortform focuses on nonfiction books. My most read genres of 2023 were finance and psychology.

If you want to read and learn more in 2024, give Shortform a try.

Using my link, you get a free trial and a 20% discount.

1. Apple Inc. (APPL)

Apple is easily one of the best businesses on the planet. It’s a masterclass example of how to build a strong brand and market new products to customers.

Since 2010, Apple has grown its revenues and cash flows by a factor of six. Net income grew even faster, going from about $14 billion in 2012 to almost $100 billion in 2023.

At the same time, they reduced the share count from 25.7 billion to 15.5 billion. They spent over $89 billion just in 2022 buying back shares. And they will continue their buyback program in the coming years. For 2024, investors expect another buyback in the $80-$90 billion range.

However, while buybacks added lots of value in the past, the current price of Apple stock might make buybacks less attractive.

Apple has a market cap of $3.046 trillion, and its growth rates have slowed significantly in recent years.

At the same time, it is valued at an LTM P/E of 32 and an NTM P/E of 30. We see the same picture looking at the LTM market cap to FCF ratio of 37. Apple is valued as a company growing double-digits in the next few years. But I doubt that they can pull this off. Of course, the buybacks will balance out the lack of growth in the coming years, but I still believe there are better investments than Apple at the current levels.

If there’s a company that deserves a premium, it’s Apple. Still, at this valuation, there are companies offering more upside potential.

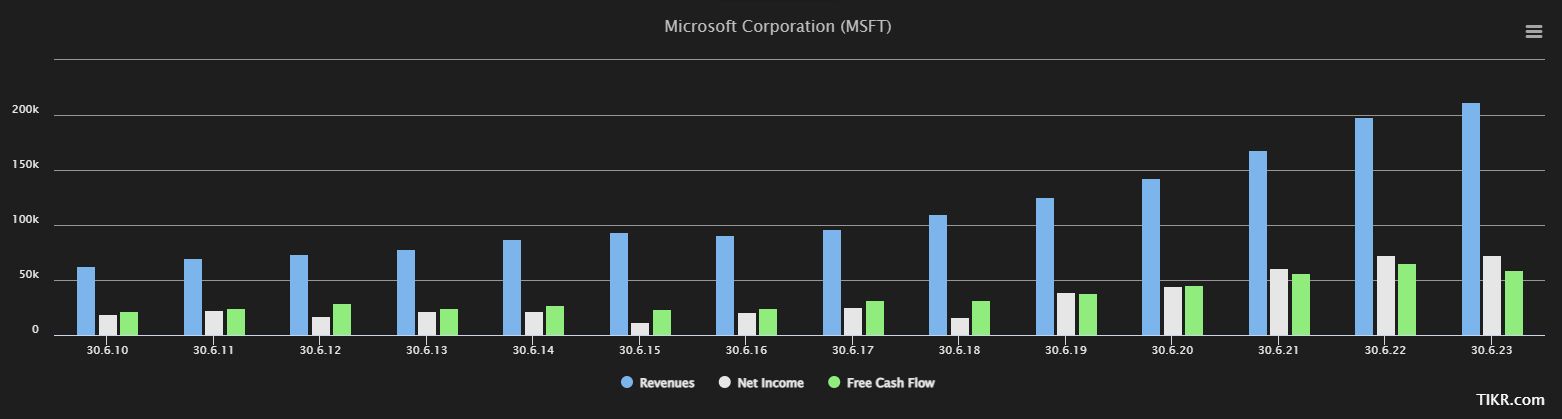

2. Microsoft Corp (MSFT)

Unsurprisingly, Microsoft, as well as Apple, is a phenomenal business. Otherwise, it wouldn’t take the second place of the S&P 500.

Since 2010, Microsoft has grown revenues by 3.4x, net income by 3.9x, and free cash flows by 2.7x. Compared to Apple, Microsoft’s growth rates are higher, and there should be more potential to grow the operational side of the business in the future.

Microsoft pays a small dividend of 0.7% and is also working on decreasing its share count. However, a lot slower than Apple. In the last 13 years, they decreased shares outstanding by 1.224 billion shares to 7.432 billion shares currently outstanding.

Microsoft stock is trading at $372, which gives Microsoft a market cap of 2.769 trillion. It trades at a LTM P/E of 36x and an NTM P/E of 33.2x.

It is equally expensive when we look at cash flow ratios. Investors are currently paying an LTM market cap to FCF of almost 55x. The conclusion is equal to Apple; the business is great, but you’re paying an expensive price.

Generally, this does not mean that Microsoft won’t perform as well over the next decade as it did over the last one. But the risk increased. You’re paying for growth in the double digits. If the stock cannot deliver on this promise, the multiples will contract.

And multiple contractions are one of the biggest risks for investors. Without the business deteriorating, the stock price could be cut in half.

Think of Apple and Microsoft not delivering the expected growth rates and being revalued at a P/E of 15. I’m not saying this is likely. But is is possible, and I don’t see how we, as investors, currently get compensated for that risk.

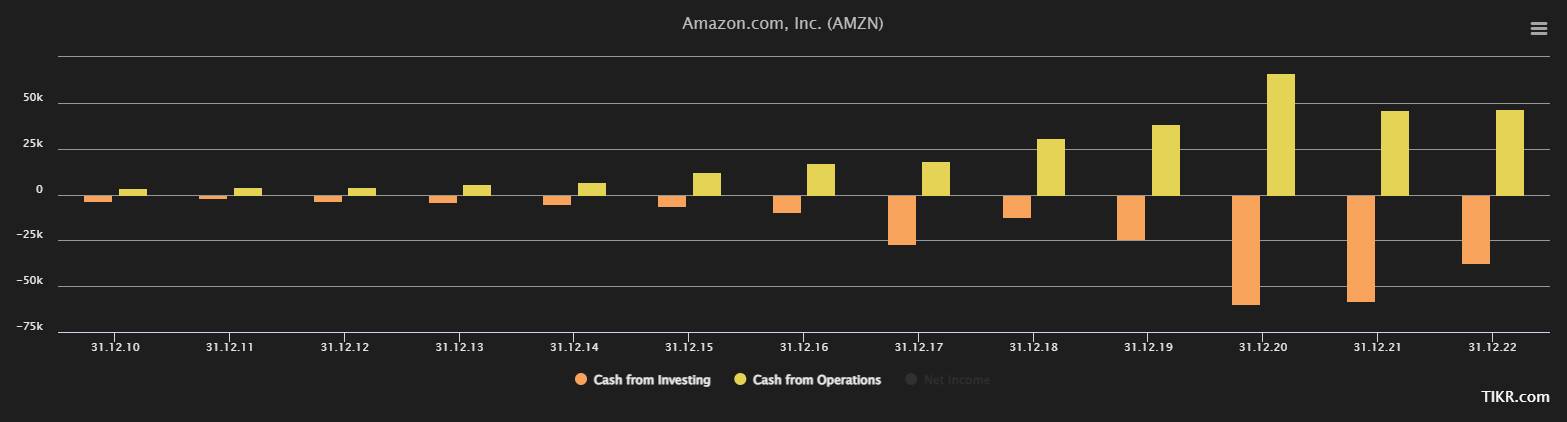

3. Amazon.com (AMZN)

Amazon marks the third of the US-Tech powerhouses. The online retailer has one of the biggest marketplaces worldwide and is the cloud market leader.

In contrast to Apple and Microsoft, Amazon is not a highly profitable company at first glance. They grew revenues by 16x(!), but their net income and cash flow growth are all over the place. Sometimes, Amazon even reports negative net income and cash flows.

However, a closer look reveals that Amazon is, in fact, a highly profitable company that chooses not to report profits and instead focuses solely on reinvesting in the business.

As you can see in the graph below, Amazon's operating cash flows are significant and constantly growing. However, Amazon invests a lot of that cash back into the business.

This strategy is the primary reason for the volatile nature of the Amazon stock.

Sometimes investors want Amazon to cut back on its investments and start to get profitable. At times of exuberance, they don’t care about cash flow or net income and appreciate Amazon’s investments.

In contrast to Apple and Microsoft, Amazon did not reach a new all-time high yet after the tech and Covid bubble burst at the end of 2022. The stock is now trading at $154 and a market cap of $1.589 trillion.

In valuation terms, this means that Amazon is trading at an LTM P/E of 80x and an NTM P/E of 46x. But as we’ve seen before, the P/E ratio is not a great tool to value Amazon since Amazon’s net income is a lot lower than it could be.

In my estimates, I expect Amazon to grow faster than Apple and Microsoft, but I still see the risk of multiple contraction as too high to invest at these levels. Once again, I believe this investment can be a good one going forward.

My concern is the lack of a margin of safety at these prices, and I believe there are opportunities better than Amazon in the current market.

I didn’t perform a DCF or reversed DCF on Amazon since its cash flows are not representative of the company’s ability to generate cash. What you could do, if you want to play with numbers, is to take the operational cash flow and adjust it for an operating margin that you consider reasonable.

4. Nvidia (NVDA)

Nvidia’s 2023 performance has been stellar, and it moved up significantly in the ranks of the S&P 500. Nvidia is the big winner of the AI revolution, and its stock tripled since the beginning of this year.

For a brief look into Nvidia’s financials, I’ve chosen a shorter timeframe, starting in 2019, than for the companies prior since most of the action happened in 2022 and 2023.

As you can see, Nvidia did, in fact, grow its financials a lot. But does this growth justify the insane stock rise? Revenues are up eightfold, net income increased from $394 million to $9.243 billion, and free cash flow rose from $695 million to $7.054 billion.

With a stock price of $481, its trading at an LTM P/E of 63x, Nvidia seems very expensive. However, if we look at the NTM P/E of “only” 24.7x, we can see that Nvidia does seem to grow in its valuation.

Taking into account the historical P/E ratios, Nvidia is in line with the level of the years prior to its stock price explosion. The current level is even slightly below the levels of 2020 to 2022.

I must say, I underestimated Nvidia’s ability to turn the AI resources that they undoubtedly had into revenues and profits this quickly. Yet, buying at this moment and at this price once again opens up the question if this is an investment that offers unlimited or at least great upside potential while being limited to the downside.

And I don’t see that at the current price and point in time. They’ve done great in the AI market, and I’m sure they will continue on that path. They generally did a great job of being the frontier of new technologies. But now it is priced into the stock.

I keep this on my watchlist and will return with a deeper analysis of the business when the sentiment is less good than it is now (Let me know if you want a Deep Dive on Nvidia). And I have the feeling we will see such sentiment sooner than most people think.

Probably not in a month or two, but who knows what happens in a year from now?

If I plug the current numbers in my Reversed DCF Model, the market is expecting Nvidia to grow FCF by 23% annually in the next 5 years and 18% annually in the five years after that. Not impossible. But it's too risky for me personally.

5. Alphabet (GOOGL)

Google just recently made headlines with its new language AI model Gemini. It is supposed to be Google’s way into the AI market, which they have mostly missed out on before, despite their great positioning through all of their data.

Like every other big tech stock, Google stock recovered from the 2022 lows and is close to the 2021 all-time highs.

Google continues to show steady growth in its financials and, like Apple, is focused on buying back shares and decreasing the share count in order to increase the share price.

The graph doesn’t show a steep decline in the share count yet because Google has only followed this share repurchase program since 2019 and increased it year by year. In 2019, they spent $18 billion on buybacks. In 2023, they spent over $60 billion buybacks.

Taking this into account, the share count should decrease a lot faster in the years ahead.

Valuation-wise, Google might be the “least-overvalued” one. If we look at the historic P/E ratios, Google is currently cheaper than it was in recent years.

The share buyback program should be another catalyst for Goodle besides the operational improvement of the business. I sold my Google stock recently and currently do not own any of the big tech companies (as you can see in My Portfolio). I had a good entry in the lows of early 2023.

But, at current prices, I’m not sure Google can meet my threshold for investing (15% per year). I think Google can get you 10% per year. If the macro environment remains stable and Google delivers on its AI promises, it could be way better.

Still, I think there are better opportunities in the micro- and small-cap sectors that I prefer from a risk-reward perspective. If you want to read about them, I wrote two analyses of such companies recently (linked below).

Once again, thanks to Shortform for sponsoring today’s episode of The All-in-One Newsletter!

Merry Christmas to anyone who celebrates! We will see each other again before New Year, so my “Happy New Year Wishes” have to wait for a bit!

My Current Portfolio:

My Stock Research:

Here’s my Investing Checklist (Free for all Paid Subscribers):

https://danielmnkeproducts.com/

Here are the tools that I use for researching Companies/Stocks: